Contango Explained: What It Means for Producers and Consumers

April 15, 2025·4 min read

Contango Explained: What It Means for Producers and Consumers

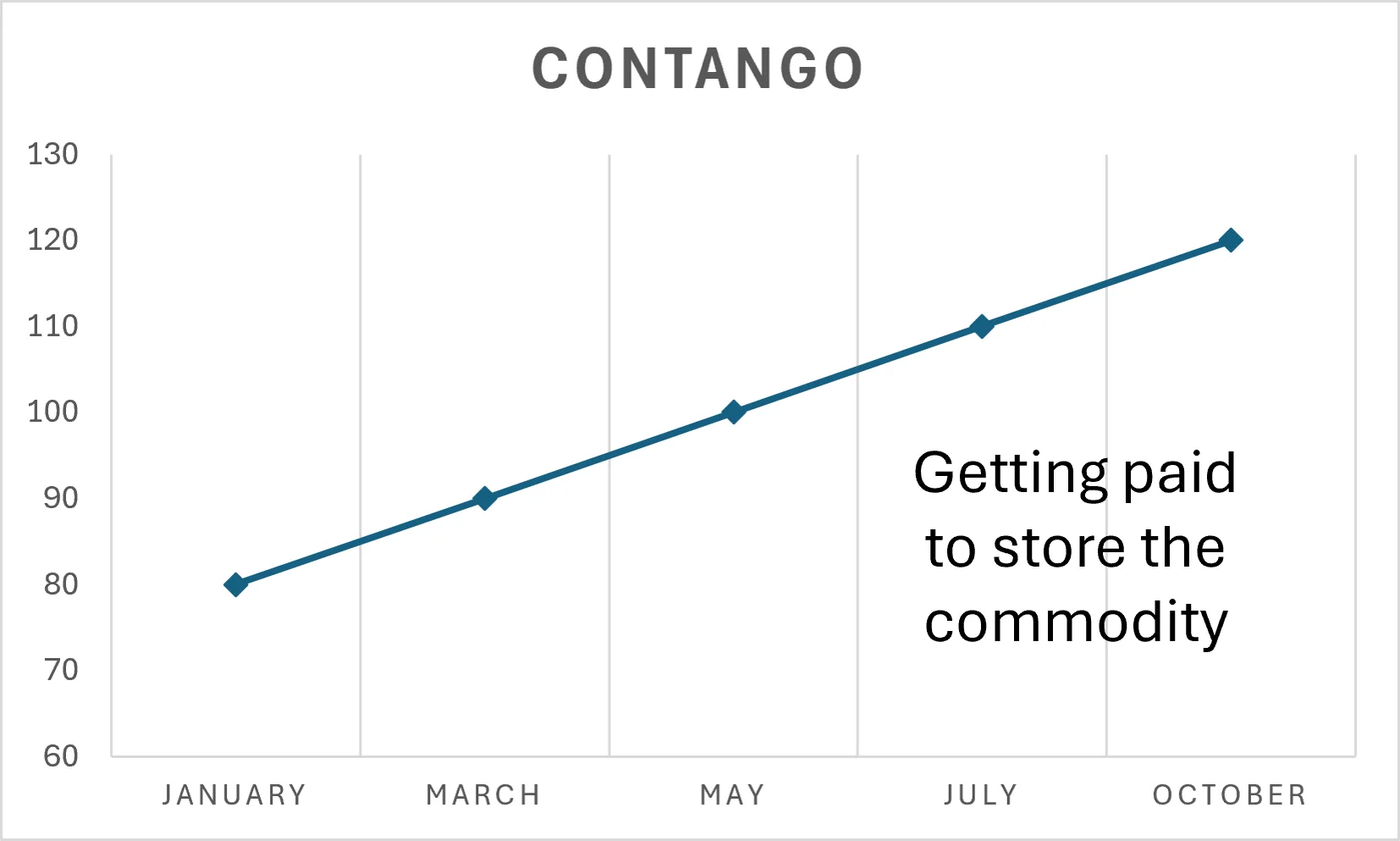

Whenever you see a futures contract trading at a price that is higher than the price of a nearby contract, you are seeing contango. Said another way, when you see the futures curve sloping upward, you are seeing contango.

For example, the March oil contract is trading at $80 per barrel and the June contract is trading at $90 per barrel. This is contango. Why would this happen?

Let's start by saying what contango is not. Contango is not the market's expectation of higher prices in the future. It's actually the opposite. When you see contango, you are seeing the market's expectation of lower prices in the future. But why would that be?

That is because the market is signaling that there is an oversupply of the commodity in the near term. It is compensating the holder for the cost of carrying and storing the commodity until a later date. How?

By storing and hedging forward, the producer can lock in $90 instead of selling now at $80, gaining $10 per barrel. So the producer is incentivized to hold inventory and deliver later. Of course, the producer must weigh storage costs against that $10 differential. The futures market does its job of price discovery, reflecting the true cost of carry and helping to ensure that the market is efficient. It is up to the producer to decide whether to store or deliver now.

Change your perspective about contango. The futures market is not in the business of predicting the future. It is in the business of discounting all information that is available today and converting that into a price that communicates the current state of things. It is in the business of price discovery, not price prediction.

What should a consumer do with a market in contango?

Take advantage of lower near-term prices. Buy spot, build inventory, and lock in near-term supply at current prices rather than hedging far forward. Why?

You'll notice that during contango, as contracts expire and new contracts take the place of 'front month', the very day that the roll occurs there is a gap up that quickly corrects and pushes the price of the new front month to align with the spot market. Playing this roll is costly for a bonafide consumer hedger who holds long futures positions — you sell the expiring contract at a lower price and roll into the next month at a higher one, losing the difference on every roll. So if you can buy physical commodity now and store it yourself, you are effectively capturing the storage trade and locking in a lower cost.

But this takes capital. I don't see consumers buying up all the inventory and paying storage costs, and I don't see consumers rushing to buy futures when market is in contango. What I see is them using options, for example, a consumer 3-way collar, where they sell an out of the money put, buy a near the money call, and sell a higher call. For longer periods, I see them just doing collars where they sell put and buy call.

Although the collar allows for some downside, there is always the risk of change in market fundamentals, causing it to fall below the put. What happens if a consumer offsets their exposure completely, at some point, the hedge might: require so much capital it becomes unsustainable, make the consumer less competitive than its peers and lose market share, or a combination of the two.

For these reasons, consumers need to have a sound risk management strategy that limits their exposure to a tolerable level, not offset it completely.

What should a producer do with a market in contango?

They know this, but here you go. Contango is a producer's best friend. The market is paying a premium for future delivery, and that is a clear invitation to lock in forward sales. A straightforward short futures position captures that premium directly. But if you still want to maintain some upside participation in case prices go even higher, a 3-way collar fits perfectly with the view: buy a near the money put, sell a lower put, and sell an out of the money call to finance the put spread. Another strategy could be sell future and sell out of the money put, the put premium is a credit which can be used to 'lift' the level of the future.

There are so many things a producer can do in this type of market.

Reach out if you want to talk about producer or consumer hedges during contango.

In the meantime, if you want to learn about the opposite of contango, check out this post: Backwardation Explained